NEXT GEN INSPIRED BY OLIVER VELEZDYOR NFA

1. Initial Setup & Application

Load the Strategy to your desired chart (e.g., EURUSD M5, as suggested by the script's backtest).

Overlay: Ensure the script is set to overlay=true (which it is) so the signals and Moving Averages plot directly on the price chart.

Equity Management: Review the initial strategy settings for capital and position sizing:

Initial Capital: Defaults to 10,000.

Default Qty Type: Set to strategy.percent_of_equity (22%), meaning 22% of your available equity is used per trade. Adjust this percentage based on your personal risk tolerance.

2. Reviewing Key Indicator Inputs

The script uses default values that are optimized, but you can adjust them in the settings panel:

Fast EMA: Defaults to 9 (e.g., a 9-period Exponential Moving Average).

Slow EMA: Defaults to 21 (e.g., a 21-period Exponential Moving Average). These EMAs define the short-term trend.

ATR: Defaults to 14 (Average True Range). Used to dynamically calculate volatility for SL/TP distances.

Final R:R: Defaults to 4.5 (minimum R:R required for a signal). This is the core of the strategy's high reward goal.

3. Interpreting Entry Signals

A trade signal is generated only when all conditions—EMA trend, "Elephant Logic" momentum, and non-ranging market—are met.

Long Signal: Appears as a green triangle (▲) below the bar, labeled "COMBO".

Short Signal: Appears as a red triangle (▼) above the bar, labeled "COMBO".

Live Plan: Upon signal, a detailed label is immediately plotted on the chart showing the FULL BATTLE PLAN:

SL: Calculated Stop Loss price.

TP: Calculated Take Profit price (based on the Final R:R).

Risk/Reward Pips: The calculated pips for the trade's risk and reward.

R:R = 1:4.5: The exact Risk-to-Reward ratio.

4. Understanding Market Conditions & Visuals

The script provides visuals to help you understand the current market state:

Trend EMAs: The 9 EMA (green) and 21 EMA (purple/magenta) are plotted to show the underlying trend.

Long trades only fire when Price > 9 EMA > 21 EMA.

Short trades only fire when Price < 9 EMA < 21 EMA.

Ranging Market (Rejection): Bars turn a light gray/silver when the proprietary "Reject Ranging" logic is active, indicating a low-volatility period. No new trades will be taken during these bars.

Momentum Bar: Bars turn a gold/yellow color when the "Elephant Logic" (high-momentum, large-body candles over 2-3 periods) is detected, highlighting powerful price movement.

5. Execution and Exit Logic

The strategy handles entry, scaling, and exit automatically:

Entry: A market order is placed (strategy.entry) immediately upon the bar where the longSetup or shortSetup condition is met.

Scaling Out (+1R): If the trade moves favorably by an amount equal to the initial risk (1R), the script closes a portion of the position (strategy.close with comment "+1R"). This partial exit locks in profit equivalent to the initial risk.

Re-entry (Pyramiding): After the +1R exit, the strategy attempts a re-entry (LONG RE/SHORT RE diamond plot) if the price meets certain criteria near the 9 EMA, trying to capitalize on further trend continuation.

Final Exits:

Take Profit: A limit order is set at the calculated TP level (stopDist * minRR).

Stop Loss: A stop order is set at the calculated SL level (stopDist * 1.3), slightly wider than the initial SL distance, likely to account for spread/slippage, ensuring the maximum loss is defined.

Trailing Stop: A trailing stop is applied to the re-entry positions (LONG RE/SHORT RE) to protect profits as the market moves further in the direction of the trade.

Search in scripts for "stop loss"

Complete DashboardPA+AI PRE/GO Trading Dashboard v0.1.2 - Publication Summary

Overview

A comprehensive multi-component trading system that combines technical analysis with an intelligent probability scoring framework to identify high-quality trade setups. The indicator features TTM Squeeze integration, volatility regime adaptation, and professional risk management tools—all presented in an intuitive 4-dashboard interface.

Key Features

🎯 8-Component Probability Scoring System (0-100%)

VWAP Position & Momentum - Price location and directional bias

MACD Alignment - Trend confirmation and momentum strength

EMA Trend Analysis - Multi-timeframe trend validation

Volume Surge Detection - Relative volume analysis (RVOL)

Price Extension Analysis - Distance from VWAP in ATR multiples

TTM Squeeze Status - Volatility compression/expansion cycles

Squeeze Momentum - Directional thrust measurement

Confluence Scoring - Multi-indicator alignment bonus

🔥 TTM Squeeze Integration

Squeeze Detection - Identifies consolidation phases (BB inside KC)

Strength Classification - Distinguishes tight vs. loose squeezes

Fire Signals - Premium entry alerts when squeeze releases

Building Alerts - Early warnings when tight squeezes are coiling

📊 Volatility Regime Adaptation

Dynamic Thresholds - Auto-adjusts based on ATR percentile (100-bar)

Three Regimes - LOW VOL, NORMAL, HIGH VOL classification

Adaptive Parameters - RVOL requirements and distance limits adjust automatically

Context-Aware Scoring - Volume expectations scale with market volatility

💰 Professional Risk Management

Position Sizing Calculator - Risk-based share calculation (% of account)

ATR Trailing Stops - Dynamic stop-loss that tightens with profits

Multiple Entry Strategies - VWAP reversion and pullback entries

Complete Trade Info - Entry, stop, target, and size for every signal

📈 Multi-Timeframe Analysis Dashboard

4 Timeframes - Daily, 4H, 15m, 5m (customizable)

6 Metrics per TF - Price change, MACD, RSI, RVOL, EMA trend

Alignment Visualization - Color-coded bull/bear indicators

HTF Context - Understand broader market structure

🛡️ Reliability Features

Confirm-on-Close - Eliminates intrabar repainting

Minimum Bars Filter - Prevents premature signals on chart load

NA-Safe Calculations - Works reliably on all symbols/timeframes

Zero Division Protection - Bulletproof math across all market conditions

What Makes This Indicator Unique

Intelligent Probability Weighting

Unlike binary "buy/sell" indicators, this system quantifies setup quality from 0-100%, allowing traders to:

Filter by confidence - Only take 70%+ probability setups

Size accordingly - Larger positions on higher probability signals

Understand context - Know exactly why a signal fired

Squeeze-Enhanced Entries

The integration of TTM Squeeze analysis adds a powerful timing dimension:

Premium Signals - 🔥 when squeeze fires + high probability (75%+)

Regular Signals - Standard entries during trending conditions

Avoid Chop - No entries during squeeze consolidation

Strength Matters - Tight squeezes (BB width <20th percentile) get bonus points

Adaptive Intelligence

The volatility regime system ensures the indicator performs across all market conditions:

Dead markets - Tighter thresholds prevent false signals

Volatile markets - Loosened requirements catch real moves

Automatic adjustment - No manual intervention needed

Dashboard-Centric Design

All critical information visible at a glance:

Top-right - Probability breakdown & regime status

Middle-right - Multi-timeframe alignment matrix

Middle-left - RVOL status (volume confirmation)

Bottom-right - Entry strategies with exact prices & sizes

Ideal For

✅ Day Traders - Intraday setups with clear entry/exit

✅ Swing Traders - Multi-timeframe confirmation for position trades

✅ Options Traders - Squeeze timing for volatility expansion plays

✅ Systematic Traders - Quantified probabilities for rule-based systems

✅ Risk Managers - Built-in position sizing & stop placement

Technical Specifications

Indicator Type: Overlay (draws on price chart)

Pine Script Version: v6

Calculation Method: Real-time, confirm-on-close option

Alerts: 8 different alert types (premium entries, exits, squeeze warnings)

Customization: 30+ input parameters

Performance: Optimized for real-time updates

Entry Strategies Included

1. VWAP Reversion

Enter when price bounces off VWAP ± 0.7 ATR

Targets mean reversion moves

Best for range-bound or choppy markets

2. Pullback to Structure

Enter on 50% retracement from swing high/low

Targets trend continuation after healthy pullback

Best for strong trending markets

Both strategies include:

Precise entry levels

ATR-based stop placement

Risk/reward targets

Position size calculation

Alert System

8 Alert Types:

🔥 Premium Long - Squeeze firing + bullish + high probability

🔥 Premium Short - Squeeze firing + bearish + high probability

🟢 High Probability Long - Standard bullish setup (70%+)

🔴 High Probability Short - Standard bearish setup (70%+)

⚡ Squeeze Coiling Long - Tight squeeze building, bullish bias

⚡ Squeeze Coiling Short - Tight squeeze building, bearish bias

Exit Long - Long position exit signal

Exit Short - Short position exit signal

Settings & Customization

Basic Settings

ATR Length (default: 14)

Confirm on Close (default: ON)

Minimum Bars Required (default: 50)

Squeeze Settings

Bollinger Band Length & Multiplier

Keltner Channel Length & Multiplier

Momentum Length

Squeeze strength classification

Probability Settings

MACD Parameters (12, 26, 9)

Volume Surge Multiplier (1.5x)

High/Medium Probability Thresholds (70%/50%)

Volatility Regime Adaptation (ON/OFF)

Risk Management

Account Equity

Risk % per Trade (default: 1%)

ATR Trailing Stop (ON/OFF)

Trail Multiplier (default: 2.0x)

Visual Settings

RVOL Period (20 bars)

Fast/Slow EMA (9/21)

Show/Hide each timeframe

Dashboard positioning

Use Cases

Conservative Trading

Set High Probability Threshold to 75%+

Enable Confirm-on-Close

Only take Premium (🔥) entries

Use 0.5% risk per trade

Aggressive Trading

Set Medium Probability Threshold to 50%

Disable Confirm-on-Close (live signals)

Take all High Probability entries

Use 1.5-2% risk per trade

Squeeze Specialist

Focus exclusively on Premium entries (squeeze firing)

Wait for "TIGHT SQUEEZE" status

Monitor squeeze building alerts

Enter immediately on fire signal

Range Trading

Use VWAP reversion entries only

Lower probability threshold to 60%

Tighter trailing stops (1.5x ATR)

Focus on low volatility regime periods

Performance Expectations

Based on backtesting and design principles:

Signal Quality:

False signals reduced ~20-30% vs. single-indicator systems

Win rate improvement ~5-10% from regime adaptation

Average win size +15-20% from trailing stops

Execution:

Clear entry signals with exact prices

Defined risk on every trade (stop loss)

Consistent position sizing (% of account)

Professional trade management

Adaptability:

Works across stocks, futures, forex, crypto

Performs in trending and ranging markets

Adjusts to changing volatility automatically

Version History

v0.1.2 (Current)

Added squeeze momentum scoring (was calculated but unused)

Implemented volatility regime adaptation

Added confluence scoring (multi-indicator alignment)

Enhanced squeeze strength classification (tight vs. loose)

Improved reliability (confirm-on-close, NA-safe calculations)

Added ATR trailing stops

Added position sizing calculator

Consolidated alert system

v0.1.1

Initial release with 6-component probability system

Basic TTM Squeeze integration

Multi-timeframe analysis

Entry strategy frameworks

Limitations & Disclaimers

⚠️ Not a Holy Grail - No indicator is 100% accurate; losses will occur

⚠️ Requires Judgment - Use probability scores to guide, not replace, decision-making

⚠️ Backtesting Recommended - Test on paper/demo before live trading

⚠️ Market Dependent - Performance varies by asset class and market conditions

⚠️ Risk Management Essential - Always use stops; never risk more than you can afford to lose

Installation & Setup

Copy the Pine Script code

Open TradingView chart

Pine Editor → Paste code → "Add to Chart"

Configure inputs for your trading style

Set up alerts via TradingView alert menu

Paper trade for 20+ signals before going live

Future Development Roadmap

Phase 3 (Planned)

HTF alignment filter (require Daily + 4H confirmation)

Session filters (avoid low-liquidity periods)

Probability decay (signals lose value over time)

Squeeze pre-alert enhancements

Phase 4 (AI Integration)

Feature vector export via webhooks

ML-based parameter optimization

Neural network regime classification

Reinforcement learning for exits

Support & Documentation

Included Documentation:

Complete changelog with implementation details

Technical guide explaining all components

Risk management best practices

Alert configuration guide

Best Practices:

Start with default settings

Enable Confirm-on-Close initially

Use 1% risk per trade or less

Focus on Premium (🔥) entries first

Keep a trade journal to track performance

Credits & Methodology

Indicators Used:

TTM Squeeze (John Carter)

VWAP (Volume-Weighted Average Price)

MACD (Gerald Appel)

Exponential Moving Averages

Average True Range (Wilder)

Relative Volume

Original Contributions:

Multi-component probability weighting system

Volatility regime adaptation framework

Confluence scoring methodology

Integrated risk management calculator

Dashboard-centric visualization

License & Terms

Usage: Free for personal trading

Modification: Open source, modify as needed

Distribution: Credit original author if sharing modified versions

Commercial Use: Contact author for licensing

No Warranty: This indicator is provided "as-is" without guarantees of profitability. Trading involves substantial risk. Past performance does not guarantee future results.

Quick Stats

📊 Components: 8

🎯 Probability Range: 0-100%

📈 Timeframes: 4 (customizable)

🔔 Alert Types: 8

⚙️ Input Parameters: 30+

📱 Dashboards: 4

💰 Entry Strategies: 2 (VWAP + Pullback)

🛡️ Risk Management: Integrated

Status: Production Ready ✅

Version: 0.1.2

Last Updated: November 2025

Pine Script: v6

File Name: PA_AI_PRE_GO_v0.1.2_FIXED.pine

One-Line Summary

A professional-grade trading dashboard combining 8 technical components with TTM Squeeze analysis, volatility-adaptive thresholds, and integrated risk management—delivering quantified probability scores (0-100%) for every trade setup.

Hybrid Linear Regression Channel with Fibonacci LevelsHow to Use the LRC Fib Hybrid Indicator (Detailed Guide)

1. Read the Trend

2.The thick blue line is the linear regression midline.

If it’s sloping upward → uptrend (favor longs).

If sloping downward → downtrend (favor shorts).

The gray channel bounds are ±2 standard deviations (adjustable).

3. Understand Fibonacci Levels

Fib lines are projected parallel to the regression slope using the channel width as 100%:

Red dashed lines (0.0 to 0.786): Support zones in uptrends.

Blue dashed line (0.5): Midline/neutral.

Green dashed lines (1.0 to 2.618): Resistance zones in downtrends.

Strongest levels: 0.618 (support) and 1.618 (resistance).

4. Buy Signal (Long Entry)

Triggered when:

Midline is rising (uptrend confirmed).

Price crosses above a red Fib level (0.0–0.786).

Volume > 20-period average (if confirmation enabled).

Action:

Enter long on the green triangle (▲).

Stop Loss: Below the lower gray channel or recent swing low.

Take Profit: At 1.0, 1.272, or 1.618 green Fibs.

5. Sell Signal (Short Entry)

Triggered when:

Midline is falling (downtrend).

Price crosses below a green Fib level (1.272–2.618).

Volume > average.

Action:

Enter short on the red triangle (▼).

Stop Loss: Above the upper gray channel.

Take Profit: At 1.0, 0.786, or 0.618 red Fibs.

6. Use the Info Table (Bottom-Right)

Shows live prices of all Fib levels, current trend ("Up"/"Down"), and signal status ("BUY"/"SELL"/"None").

7. Customize via Settings (Gear Icon)

Regression Length: 50–200 (shorter = faster response).

Std Dev Multiplier: 1.5–3.0 (tighter/wider channel).

Toggle Fibs: Hide unused levels to declutter.

Volume Confirmation: Turn off for pure price action.

8. Set Alerts

Right-click chart → Add Alert → Select "Buy Signal" or "Sell Signal" → Enable popup/email/webhook.

9. Best Practices

Best in trending markets (avoid chop).

Wait for volume spike on bounce.

Combine with higher timeframe bias.

Use 0.618/1.618 as primary reversal zones.

This indicator gives you adaptive trend, precise entries, volume filter, and dynamic targets — all in one clean overlay.

v2.0—Tristan's Multi-Indicator Reversal Strategy🎯 Multi-Indicator Reversal Strategy - Optimized for High Win Rates

A powerful confluence-based strategy that combines RSI, MACD, Williams %R, Bollinger Bands, and Volume analysis to identify high-probability reversal points . Designed to let winners run with no stop loss or take profit - positions close only when opposite signals occur.

Also, the 3 hour timeframe works VERY well—just a lot less trades.

📈 Proven Performance

This strategy has been backtested and optimized on multiple blue-chip stocks with 80-90%+ win rates on 1-hour timeframes from Aug 2025 through Oct 2025:

✅ V (Visa) - Payment processor

✅ MSFT (Microsoft) - Large-cap tech

✅ WMT (Walmart) - Retail leader

✅ IWM (Russell 2000 ETF) - Small-cap index

✅ NOW (ServiceNow) - Enterprise software

✅ WM (Waste Management) - Industrial services

These stocks tend to mean-revert at extremes, making them ideal candidates for this reversal-based approach. I only list these as a way to show you the performance of the script. These values and stock choices may change over time as the market shifts. Keep testing!

🔑 How to Use This Strategy Successfully

Step 1: Apply to Chart

Open your desired stock (V, MSFT, WMT, IWM, NOW, WM recommended)

Set timeframe to 1 Hour

Apply this strategy

Check that the Williams %R is set to -20 and -80, and "Flip All Signals" is OFF (can flip this for some stocks to perform better.)

Step 2: Understand the Signals

🟢 Green Triangle (BUY) Below Candle:

Multiple indicators (RSI, Williams %R, MACD, Bollinger Bands) show oversold conditions

Enter LONG position

Strategy will pyramid up to 10 entries if more buy signals occur

Hold until red triangle appears

🔴 Red Triangle (SELL) Above Candle:

Multiple indicators show overbought conditions

Enter SHORT position (or close existing long)

Strategy will pyramid up to 10 entries if more sell signals occur

Hold until green triangle appears

🟣 Purple Labels (EXIT):

Shows when positions close

Displays count if multiple entries were pyramided (e.g., "Exit Long x5")

Step 3: Let the Strategy Work

Key Success Principles:

✅ Be Patient - Signals don't occur every day, wait for quality setups

✅ Trust the Process - Don't manually close positions, let opposite signals exit

✅ Watch Pyramiding - The strategy can add up to 10 positions in the same direction

✅ No Stop Loss - Positions ride through drawdowns until reversal confirmed

✅ Session Filter - Only trades during NY session (9:30 AM - 4:00 PM ET)

⚙️ Winning Settings (Already Set as Defaults)

INDICATOR SETTINGS:

- RSI Length: 14

- RSI Overbought: 70

- RSI Oversold: 30

- MACD: 12, 26, 9 (standard)

- Williams %R Length: 14

- Williams %R Overbought: -20 ⭐ (check this! And adjust to your liking)

- Williams %R Oversold: -80 ⭐ (check this! And adjust to your liking)

- Bollinger Bands: 20, 2.0

- Volume MA: 20 periods

- Volume Multiplier: 1.5x

SIGNAL REQUIREMENTS:

- Min Indicators Aligned: 2

- Require Divergence: OFF

- Require Volume Spike: OFF

- Require Reversal Candle: OFF

- Flip All Signals: OFF ⭐

RISK MANAGEMENT:

- Use Stop Loss: OFF ⭐⭐⭐

- Use Take Profit: OFF ⭐⭐⭐

- Allow Pyramiding: ON ⭐⭐⭐

- Max Pyramid Entries: 10 ⭐⭐⭐

SESSION FILTER:

- Trade Only NY Session: ON

- NY Session: 9:30 AM - 4:00 PM ET

**⭐ = Critical settings for success**

## 🎓 Strategy Logic Explained

### **How It Works:**

1. **Multi-Indicator Confluence**: Waits for at least 2 out of 4 technical indicators to align before generating signals

2. **Oversold = Buy**: When RSI < 30, Williams %R < -80, price below lower Bollinger Band, and/or MACD turning bullish → BUY signal

3. **Overbought = Sell**: When RSI > 70, Williams %R > -20, price above upper Bollinger Band, and/or MACD turning bearish → SELL signal

4. **Pyramiding Power**: As trend continues and more signals fire in the same direction, adds up to 10 positions to maximize gains

5. **Exit Only on Reversal**: No arbitrary stops or targets - only exits when opposite signal confirms trend change

6. **Session Filter**: Only trades during liquid NY session hours to avoid overnight gaps and low-volume periods

### **Why No Stop Loss Works:**

Traditional reversal strategies fail because they:

- Get stopped out too early during normal volatility

- Miss the actual reversal that happens later

- Cut winners short with tight take profits

This strategy succeeds because it:

- ✅ Rides through temporary noise

- ✅ Captures full reversal moves

- ✅ Uses multiple indicators for confirmation

- ✅ Pyramids into winning positions

- ✅ Only exits when technical picture completely reverses

---

## 📊 Understanding the Display

**Live Indicator Counter (Top Corner / end of current candles):**

Bull: 2/4

Bear: 0/4

(STANDARD)

Shows how many indicators currently align bullish/bearish

"STANDARD" = normal reversal mode (buy oversold, sell overbought)

"FLIPPED" = momentum mode if you toggle that setting

Visual Indicators:

🔵 Blue background = NY session active (trading window)

🟡 Yellow candle tint = Volume spike detected

💎 Aqua diamond = Bullish divergence (price vs RSI)

💎 Fuchsia diamond = Bearish divergence

⚡ Advanced Tips

Optimizing for Different Stocks:

If Win Rate is Low (<50%):

Try toggling "Flip All Signals" to ON (switches to momentum mode)

Increase "Min Indicators Aligned" to 3 or 4

Turn ON "Require Divergence"

Test on different timeframe (4-hour or daily)

If Too Few Signals:

Decrease "Min Indicators Aligned" to 2

Turn OFF all requirement filters

Widen Williams %R bands to -15 and -85

If Too Many False Signals:

Increase "Min Indicators Aligned" to 3 or 4

Turn ON "Require Divergence"

Turn ON "Require Volume Spike"

Reduce Max Pyramid Entries to 5

Stock Selection Guidelines:

Best Suited For:

Large-cap stable stocks (V, MSFT, WMT)

ETFs (IWM, SPY, QQQ)

Stocks with clear support/resistance

Mean-reverting instruments

Avoid:

Ultra low-volume penny stocks

Extremely volatile crypto (try traditional settings first)

Stocks in strong one-directional trends lasting months

🔄 The "Flip All Signals" Feature

If backtesting shows poor results on a particular stock, try toggling "Flip All Signals" to ON:

STANDARD Mode (OFF):

Buy when oversold (reversal strategy)

Sell when overbought

May work best for: V, MSFT, WMT, IWM, NOW, WM

FLIPPED Mode (ON):

Buy when overbought (momentum strategy)

Sell when oversold

May work best for: Strong trending stocks, momentum plays, crypto

Test both modes on your stock to see which performs better!

📱 Alert Setup

Create alerts to notify you of signals:

📊 Performance Expectations

With optimized settings on recommended stocks:

Typical results we are looking for:

Win Rate: 70-90%

Average Winner: 3-5%

Average Loser: 1-3%

Signals Per Week: 1-3 on 1-hour timeframe

Hold Time: Several hours to days

Remember: Past performance doesn't guarantee future results. Always use proper risk management.

Advanced Psychological Levels with Dynamic Spacing═══════════════════════════════════════

ADVANCED PSYCHOLOGICAL LEVELS WITH DYNAMIC SPACING

═══════════════════════════════════════

A comprehensive psychological price level indicator that automatically identifies and displays round number levels across multiple timeframes. Features dynamic ATR-based spacing, smart crypto detection, distance tracking, and customizable alert system.

───────────────────────────────────────

WHAT THIS INDICATOR DOES

───────────────────────────────────────

This indicator automatically draws psychological price levels (round numbers) that often act as support and resistance:

- Dynamic ATR-Based Spacing - Adapts level spacing to market volatility

- Multiple Level Types - Major (250 pip), Standard (100 pip), Mid, and Intraday levels

- Smart Asset Detection - Automatically adjusts for Forex, Crypto, Indices, and CFDs

- Crypto Price Adaptation - Intelligent level spacing based on cryptocurrency price magnitude

- Distance Information Table - Real-time percentage distance to nearest levels

- Combined Level Labels - Clear identification when multiple level types coincide

- Performance Optimized - Configurable visible range and label limits

- Comprehensive Alerts - Notifications when price crosses any level type

───────────────────────────────────────

HOW IT WORKS

───────────────────────────────────────

PSYCHOLOGICAL LEVELS CONCEPT:

Psychological levels are round numbers where traders tend to place orders, creating natural support and resistance zones. These include:

- Forex: 1.0000, 1.0100, 1.0050 (pips)

- Crypto: $100, $1,000, $10,000 (whole numbers)

- Indices: 10,000, 10,500, 11,000 (points)

Why They Matter:

- Traders naturally gravitate to round numbers

- Stop losses cluster at these levels

- Take profit orders concentrate here

- Institutional algorithmic trading often targets these levels

DYNAMIC ATR-BASED SPACING:

Traditional Method:

- Fixed spacing regardless of volatility

- May be too tight in volatile markets

- May be too wide in quiet markets

Dynamic Method (Recommended):

- Uses ATR (Average True Range) to measure volatility

- Automatically adjusts level spacing

- Tighter levels in low volatility

- Wider levels in high volatility

Calculation:

1. Calculate ATR over specified period (default: 14)

2. Multiply by ATR multiplier (default: 2.0)

3. Round to nearest psychological level

4. Generate levels at dynamic intervals

Benefits:

- Adapts to market conditions

- More relevant levels in all volatility regimes

- Reduces clutter in trending markets

- Provides more detail in ranging markets

LEVEL TYPES:

Major Levels (250 pip/point):

- Highest significance

- Primary support/resistance zones

- Color: Red (default)

- Style: Solid lines

- Spacing: 2.5x standard step

Standard Levels (100 pip/point):

- Secondary importance

- Common psychological barriers

- Color: Blue (default)

- Style: Dashed lines

- Spacing: Standard step

Mid Levels (50% between major):

- Optional intermediate levels

- Halfway between major levels

- Color: Gray (default)

- Style: Dotted lines

- Usage: Additional confluence points

Intraday Levels (sub-100 pip):

- For intraday traders

- Fine-grained precision

- Color: Yellow (default)

- Style: Dotted lines

- Only shown on intraday timeframes

SMART ASSET DETECTION:

Forex Pairs:

- Detects major currency pairs automatically

- Uses pip-based calculations

- Standard: 100 pips (0.0100)

- Major: 250 pips (0.0250)

- Intraday: 20, 50, 80 pip subdivisions

Cryptocurrencies:

- Automatic price magnitude detection

- Adaptive spacing based on price:

* Under $0.10: Levels at $0.01, $0.05

* $0.10-$1: Levels at $0.10, $0.50

* $1-$10: Levels at $1, $5

* $10-$100: Levels at $10, $50

* $100-$1,000: Levels at $100, $500

* $1,000-$10,000: Levels at $1,000, $5,000

* Over $10,000: Levels at $5,000, $10,000

Indices & CFDs:

- Fixed point-based system

- Major: 500 point intervals (with 250 sub-levels)

- Standard: 100 point intervals

- Suitable for stock indices like SPX, NASDAQ

COMBINED LEVEL LABELS:

When multiple level types coincide at the same price:

- Single line drawn (highest priority color)

- Combined label shows all types

- Priority: Major > Standard > Mid > Intraday

Example Label Formats:

- "1.1000 Major" - Major level only

- "1.1000 Std + Major" - Both standard and major

- "50000 Intra + Mid + Std" - Three levels coincide

Benefits:

- Cleaner chart appearance

- Clear identification of confluence

- Reduced visual clutter

- Easy to spot high-importance levels

DISTANCE INFORMATION TABLE:

Real-time tracking of nearest levels:

Table Contents:

- Nearest major level above (price and % distance)

- Nearest standard level above (price and % distance)

- Nearest standard level below (price and % distance)

Display:

- Top right corner (configurable)

- Color-coded by level type

- Real-time percentage calculations

- Helpful for position management

Usage:

- Identify proximity to key levels

- Set realistic profit targets

- Gauge potential move magnitude

- Monitor approaching resistance/support

ALERT SYSTEM:

Comprehensive crossing alerts:

Alert Types:

- Major Level Crosses

- Standard Level Crosses

- Intraday Level Crosses

Alert Modes:

- First Cross Only: Alert once when level is crossed

- All Crosses: Alert every time level is crossed

Alert Information:

- Level type crossed

- Specific price level

- Direction (above/below)

- One alert per bar to prevent spam

Configuration:

- Enable/disable by level type

- Choose alert frequency

- Customize for your trading style

───────────────────────────────────────

HOW TO USE

───────────────────────────────────────

INITIAL SETUP:

General Settings:

1. Enable "Use Dynamic ATR-Based Spacing" (recommended)

2. Set ATR Period (14 is standard)

3. Adjust ATR Multiplier (2.0 is balanced)

Visibility Settings:

1. Set Visible Range % (10% recommended for clarity)

2. Adjust Label Offset for readability

3. Configure performance limits if needed

Level Selection:

1. Enable/disable level types based on trading style

2. Adjust line counts for each type

3. Choose line styles and colors for visibility

TRADING STRATEGIES:

Breakout Trading:

1. Wait for price to approach major or standard level

2. Monitor for consolidation near level

3. Enter on confirmed break above/beyond level

4. Stop loss just beyond the broken level

5. Target: Next major or standard level

Rejection Trading:

1. Identify major psychological level

2. Wait for price to test the level

3. Look for rejection signals (wicks, bearish/bullish candles)

4. Enter in direction of rejection

5. Stop beyond the level

6. Target: Previous level or mid-level

Range Trading:

1. Identify range between two major levels

2. Buy at lower psychological level

3. Sell at upper psychological level

4. Use standard and mid-levels for position management

5. Exit if major level breaks with volume

Confluence Trading:

1. Look for combined levels (Std + Major)

2. These represent high-probability zones

3. Use as primary support/resistance

4. Increase position size at confluence

5. Expect stronger reactions at these levels

Session-Based Trading:

1. Note opening level at session start (Asian/London/NY)

2. Trade breakouts of major levels during high-volume sessions

3. London/NY sessions: More likely to break levels

4. Asian session: More likely to respect levels (range trading)

RISK MANAGEMENT WITH PSYCHOLOGICAL LEVELS:

Stop Loss Placement:

- Place stops just beyond psychological levels

- Add buffer (5-10 pips for forex)

- Avoid exact round numbers (stop hunting risk)

- Use previous major level as maximum stop

Take Profit Strategy:

- First target: Next standard level (partial profit)

- Second target: Next major level (remaining position)

- Trail stops to breakeven at first target

- Use distance table to calculate risk/reward

Position Sizing:

- Larger positions at major levels (higher probability)

- Smaller positions at intraday levels (lower probability)

- Scale in at standard levels between major levels

- Reduce size when multiple levels are close together

TIMEFRAME CONSIDERATIONS:

Higher Timeframes (4H, Daily, Weekly):

- Focus on Major and Standard levels only

- Disable Intraday and Mid levels

- Wider level spacing expected

- Use for swing trading and position trading

Lower Timeframes (5m, 15m, 1H):

- Enable all level types

- Use Intraday levels for precision

- Tighter level spacing acceptable

- Good for day trading and scalping

Multi-Timeframe Approach:

- Identify major levels on Daily/4H charts

- Refine entries using 15m/1H intraday levels

- Trade in direction of higher timeframe bias

- Use lower timeframe levels for position management

───────────────────────────────────────

CONFIGURATION GUIDE

───────────────────────────────────────

GENERAL SETTINGS:

Dynamic ATR-Based Spacing:

- Enabled: Recommended for most markets

- Disabled: Fixed psychological levels

- ATR Period: 14 (standard), 10 (responsive), 20 (smooth)

- ATR Multiplier: 1.0-5.0 (2.0 is balanced)

VISIBILITY SETTINGS:

Visible Range %:

- 5%: Very tight range, minimal clutter

- 10%: Balanced view (recommended)

- 20%: Wide range, more context

- 50%: Maximum range, all levels visible

Label Offset:

- 10-20 bars: Close to current price

- 30-50 bars: Moderate distance

- 50-100 bars: Far from price action

Performance Limits:

- Max Historical Bars: Reduce if indicator loads slowly

- Max Labels: Reduce for cleaner chart (20-30 recommended)

LEVEL CUSTOMIZATION:

Line Count:

- Lower (1-3): Cleaner chart, fewer levels

- Medium (4-6): Balanced view

- Higher (7-10): More context, busier chart

Line Styles:

- Solid: High importance, easy to see

- Dashed: Medium importance, clear but subtle

- Dotted: Low importance, minimal visual weight

Colors:

- Use contrasting colors for different level types

- Red/Blue/Yellow default works well

- Adjust based on chart background and personal preference

DISTANCE TABLE:

Position:

- Top Right: Doesn't interfere with price action

- Top Left: Good for right-side price scale

- Bottom positions: Less common but available

Colors:

- Default (white text, dark background) works for most charts

- Match your chart theme for consistency

- Ensure text is readable against background

ALERT CONFIGURATION:

Alert by Level Type:

- Major: Most important, fewer false signals

- Standard: Balance of frequency and importance

- Intraday: Many signals, best for active traders

Alert Frequency:

- First Cross Only: Cleaner, less noise (recommended for swing trading)

- All Crosses: Every touch, good for scalping

Alert Setup in TradingView:

1. Configure desired alert types in indicator settings

2. Right-click chart → Add Alert

3. Select this indicator

4. Choose "Any alert() function call"

5. Set delivery method (mobile, email, webhook)

───────────────────────────────────────

ASSET-SPECIFIC TIPS

───────────────────────────────────────

FOREX (EUR/USD, GBP/USD, etc.):

- Major levels at x.x000, x.x500

- Standard levels at x.xx00

- Intraday levels at 20/50/80 pips

- Most effective during London/NY sessions

- Watch for "figure" levels (1.0000, 1.1000)

CRYPTOCURRENCIES (BTC, ETH, etc.):

- Enable dynamic spacing for volatile markets

- Levels adjust automatically based on price

- Watch major $1,000 increments for BTC

- $100 levels important for ETH

- Smaller caps: Use standard levels

- High volatility: Increase ATR multiplier to 3.0

STOCK INDICES (SPX, NASDAQ, etc.):

- 100-point levels most important

- 500-point levels for major S/R

- 50-point mid-levels for refinement

- Watch end-of-day for level reactions

- Futures often lead spot on level breaks

GOLD/COMMODITIES:

- Major levels at $50 increments ($1,900, $1,950)

- Standard levels at $10 increments

- Very reactive to psychological levels

- Watch for false breaks during low volume

- Best reactions during active trading hours

───────────────────────────────────────

BEST PRACTICES

───────────────────────────────────────

Chart Setup:

- Use clean price action charts

- Avoid too many indicators

- Ensure psychological levels are clearly visible

- Match colors to your chart theme

Level Selection:

- Start with Major and Standard levels only

- Add Mid and Intraday as needed

- Less is more - avoid chart clutter

- Adjust based on timeframe

Combining with Other Tools:

- Volume profile for confluence

- Trendlines intersecting psychological levels

- Moving averages near round numbers

- Fibonacci levels coinciding with psychological levels

Common Mistakes to Avoid:

- Trading every level touch (be selective)

- Ignoring volume confirmation

- Setting stops exactly at levels (stop hunting)

- Forgetting to adjust for different assets

- Over-relying on levels without price action confirmation

Performance Optimization:

- Reduce visible range for faster loading

- Lower max historical bars on lower timeframes

- Limit labels to 30-50 for clarity

- Disable unused level types

───────────────────────────────────────

EDUCATIONAL DISCLAIMER

───────────────────────────────────────

This indicator identifies psychological price levels based on round numbers that tend to act as support and resistance. The methodology includes:

- Round number detection algorithms

- ATR-based dynamic spacing calculations

- Asset-specific level determination

- Distance percentage calculations

Psychological levels are a recognized concept in technical analysis, studied by traders and institutions. However, they do not guarantee price reactions and should be used as part of a comprehensive trading strategy including proper risk management, volume analysis, and price action confirmation.

───────────────────────────────────────

USAGE DISCLAIMER

───────────────────────────────────────

This tool is for educational and analytical purposes. Psychological levels can act as support or resistance but price reactions are not guaranteed. Dynamic spacing may generate different levels in different market conditions. Always conduct independent analysis, use proper risk management, and never risk capital you cannot afford to lose. Past performance does not indicate future results.

───────────────────────────────────────

CREDITS & ATTRIBUTION

───────────────────────────────────────

Original Concept: Sonar Lab

Mean Reversion Trading V1Overview

This is a simple mean reversion strategy that combines RSI, Keltner Channels, and MACD Histograms to predict reversals. Current parameters were optimized for NASDAQ 15M and performance varies depending on asset. The strategy can be optimized for specific asset and timeframe.

How it works

Long Entry (All must be true):

1. RSI < Lower Threshold

2. Close < Lower KC Band

3. MACD Histogram > 0 and rising

4. No open trades

Short Entry (All must be true):

1. RSI > Upper Threshold

2. Close > Upper KC Band

3. MACD Histogram < 0 and falling

4. No open trades

Long Exit:

1. Stop Loss: Average position size x ( 1 - SL percent)

2. Take Profit: Average position size x ( 1 + TP percent)

3. MACD Histogram crosses below zero

Short Exit:

1. Stop Loss: Average position size x ( 1 + SL percent)

2. Take Profit: Average position size x ( 1 - TP percent)

3. MACD Histogram crosses above zero

Settings and parameters are explained in the tooltips.

Important

Initial capital is set as 100,000 by default and 100 percent equity is used for trades

Adaptive Trend 1m ### Overview

The "Adaptive Trend Impulse Parallel SL/TP 1m Realistic" strategy is a sophisticated trading system designed specifically for high-volatility markets like cryptocurrencies on 1-minute timeframes. It combines trend-following with momentum filters and adaptive parameters to dynamically adjust to market conditions, ensuring more reliable entries and risk management. This strategy uses SuperTrend for primary trend detection, enhanced by MACD, RSI, Bollinger Bands, and optional volume spikes. It incorporates parallel stop-loss (SL) and multiple take-profit (TP) levels based on ATR, with options for breakeven and trailing stops after the first TP. Optimized for realistic backtesting on short timeframes, it avoids over-optimization by adapting indicators to market speed and efficiency.

### Principles of Operation

The strategy operates on the principle of adaptive impulse trading, where entry signals are generated only when multiple conditions align to confirm a strong trend reversal or continuation:

1. **Trend Detection (SuperTrend)**: The core signal comes from an adaptive SuperTrend indicator. It calculates upper and lower bands using ATR (Average True Range) with dynamic periods and multipliers. A buy signal occurs when the price crosses above the lower band (from a downtrend), and a sell signal when it crosses below the upper band (from an uptrend). Adaptation is based on Rate of Change (ROC) to measure market speed, shortening periods in fast markets for quicker responses.

2. **Momentum and Trend Filters**:

- **MACD**: Uses adaptive fast and slow lengths. In "Trend Filter" mode (default when "Use MACD Cross" is false), it checks if the MACD line is above/below the signal for long/short. In cross mode, it requires a crossover/crossunder.

- **RSI**: Adaptive period RSI must be above 50 for longs and below 50 for shorts, confirming overbought/oversold conditions dynamically.

- **Bollinger Bands (BB)**: Depending on the mode ("Midline" by default), it requires the price to be above/below the BB midline for longs/shorts, or a breakout in "Breakout" mode. Deviation adapts to market efficiency.

- **Volume Spike Filter** (optional): Entries require volume to exceed an adaptive multiple of its SMA, signaling strong impulse.

3. **Volatility Filter**: Entries are only allowed if current ATR percentage exceeds a historical minimum (adaptive), preventing trades in low-volatility ranges.

4. **Risk Management (Parallel SL/TP)**:

- **Stop-Loss**: Set at an adaptive ATR multiple below/above entry for long/short.

- **Take-Profits**: Three levels at adaptive ATR multiples, with partial position closures (e.g., 51% at TP1, 25% at TP2, remainder at TP3).

- **Post-TP1 Features**: Optional breakeven moves SL to entry after TP1. Trailing SL uses BB midline as a dynamic trail.

- All levels are calculated per trade using the ATR at entry, making them "realistic" for 1m charts by widening SL and tightening initial TPs.

The strategy enters long on buy signals with all filters met, and short on sell signals. It uses pyramid margin (100% long/short) for full position sizing.

Adaptation is driven by:

- **Market Speed (normSpeed)**: Based on ROC, tightens multipliers in volatile periods.

- **Efficiency Ratio (ER)**: Measures trend strength, adjusting periods for trending vs. ranging markets.

This ensures the strategy "adapts" without manual tweaks, reducing false signals in varying conditions.

### Main Advantages

- **Adaptability**: Unlike static strategies, parameters dynamically adjust to market volatility and trend strength, improving performance across ranging and trending phases without over-optimization.

- **Realistic Risk Management for 1m**: Wider SL and tiered TPs prevent premature stops in noisy short-term charts, while partial profits lock in gains early. Breakeven/trailing options protect profits in extended moves.

- **Multi-Filter Confirmation**: Combines trend, momentum, and volume for high-probability entries, reducing whipsaws. The volatility filter avoids flat markets.

- **Debug Visualization**: Built-in plots for signals, levels, and component checks (when "Show Debug" is enabled) help users verify logic on charts.

- **Efficiency**: Low computational load, suitable for real-time trading on TradingView with alerts.

Backtesting shows robust results on volatile assets, with a focus on sustainable risk (e.g., SL at 3x ATR avoids excessive drawdowns).

### Uniqueness

What sets this strategy apart is its **fully adaptive framework** integrating multiple indicators with real-time market metrics (ROC for speed, ER for efficiency). Most trend strategies use fixed parameters, leading to poor adaptation; here, every key input (periods, multipliers, deviations) scales dynamically within bounds, creating a "self-tuning" system. The "parallel SL/TP with 1m realism" adds custom handling for micro-timeframes: tightened initial TPs for quick wins and adaptive min-ATR filter to skip low-vol bars. Unlike generic mashups, it justifies the combination—SuperTrend for trend, MACD/RSI/BB for impulse confirmation, volume for conviction—working synergistically to capture "trend impulses" while filtering noise. The post-TP1 breakeven/trailing tied to BB adds a unique profit-locking mechanism not common in open-source scripts.

### Recommended Settings

These settings are optimized and recommended for trading ASTER/USDT on Bybit, with 1-minute chart, x10 leverage, and cross margin mode. They provide a balanced risk-reward for this volatile pair:

- **Base Inputs**:

- Base ATR Period: 10

- Base SuperTrend ATR Multiplier: 2.5

- Base MACD Fast: 8

- Base MACD Slow: 17

- Base MACD Signal: 6

- Base RSI Period: 9

- Base Bollinger Period: 12

- Bollinger Deviation: 1.8

- Base Volume SMA Period: 19

- Base Volume Spike Multiplier: 1.8

- Adaptation Window: 54

- ROC Length: 10

- **TP/SL Settings**:

- Use Stop Loss: True

- Base SL Multiplier (ATR): 3

- Use Take Profits: True

- Base TP1 Multiplier (ATR): 5.5

- Base TP2 Multiplier (ATR): 10.5

- Base TP3 Multiplier (ATR): 19

- TP1 % Position: 51

- TP2 % Position: 25

- Breakeven after TP1: False

- Trailing SL after TP1: False

- Base Min ATR Filter: 0.001

- Use Volume Spike Filter: True

- BB Condition: Midline

- Use MACD Cross (false=Trend Filter): True

- Show Debug: True

For backtesting, use initial capital of 30 USD, base currency USDT, order size 100 USDT, pyramiding 1, commission 0.1%, slippage 0 ticks, long/short margin 0%.

Always backtest on your platform and use risk management—risk no more than 1-2% per trade. This is not financial advice; trade at your own risk.

GRG/RGR Signal, MA, Ranges and PivotsThis indicator is a combination of several indicators.

It is a combination of two of my indicators which I solely use for trading

1. EMA 10-20-50-200, Pivots and Previous Day/Week/Month range

2. 3/4-Bar GRG / RGR Pattern (Conditional 4th Candle)

You can use them individually if you already have some of them or just use this one. Belive me when I say, this is all you need, along with market structure knowlege and even if you don’t have that, this indicator has been doing wonders for me. This is all I use. I do not use anything else.

**Note - Do checkout the indicators individually as I have added valuable information in the comment section.

It contains the following,

1. 10 EMA/SMA - configurable

2. 20 EMA/SMA - configurable

3. 50 EMA/SMA - configurable

4. 200 EMA/SMA - configurable

5. Previous Day's Range - configurable

6. Previous Week's Range - configurable

7. Previous Month's Range - configurable

8. Pivots - configurable

9. Buy Sell Signal - configurable

The Moving Averages

It is a very important combination and using it correctly with price action will strengthen your entries and exits.

The ema's or sma's added are the most powerful ones and they do definitely act as support and resistance.

The Daily/Weekly/Monthly Ranges

The Daily/Weekly/Monthly ranges are extremely important for any trader and should be used for targets and reversals.

Pivots

Pivots can provide support and resistance level. R5 and S5 can be used to check for over stretched conditions. You can customise them however you like. It is a full pivot indicator.

It is defaulted to show R5 and S5 only to reduce noise in the chart but it can be customised.

The 3/4 RGR or GRG Signal Generator

Combined with a 3/4 RGR or GRG setup can be all a trader needs.

You don't need complex strategies and SMC concepts to trade. Simple EMAs, ranges and RGR/GRG setup is the most winning combination.

This indicator can be used to identify the Green-Red-Green or Red-Green-Red pattern.

It is a price action indicator where a price action which identifies the defeat of buyers and sellers.

If the buyers comprehensively defeat the sellers then the price moves up and if the sellers defeat the buyers then the price moves down.

In my trading experience this is what defines the price movement.

It is a 3 or 4 candle pattern, beyond that i.e, 5 or more candles could mean a very sideways market and unnecessary signal generation.

How does it work?

Upside/Green signal

1. Say candle 1 is Green, which means buyers stepped in, then candle 2 is Red or a Doji, that means sellers brought the price down. Then if candle 3 is forming to be Green and breaks the closing of the 1st candle and opening of the 2nd candle, then a green arrow will appear and that is the place where you want to take your trade.

2. Here the buyers defeated the sellers.

3. Sometimes candle 3 falls short but candle 4 breaks candle 1's closing and candle 2's opening price. We can enter on candle 4.

4. Important - We need to enter the trade as soon as the price moves above the candle 1 and 2's body and should not wait for the 3rd or 4th candle to close. Ignore wicks.

5. But for a more optimised entry I have added an option to use candle’s highs and lows instead of open and close. This reduces lot of noise and provides us with more precise entry. This setting is turned on by default.

6. I have restricted it to 4 candles and that is all that is needed. More than that is a longer sideways market.

7. I call it the +-+ or GRG pattern or Green-Red-Green or Buyer-Seller-Buyer or Seller defeated or just Buyer pattern.

8. Stop loss can be candle 2's mid for safe traders (that includes me) or candle 2's body low for risky traders.

9. Back testing suggests that body low will be useless and result in more points in loss because for the bigger move this point will not be touched, so why not get out faster.

Downside/Red signal

1. Say candle 1 is Red, which means sellers stepped in, then candle 2 is Green or a Doji, that means buyers took the price up. Then if candle 3 is forming to be Red and breaks the closing of the 1st candle and opening of the 2nd candle then a Red arrow will appear and that is the place where you want to take your trade.

2. Sometimes candle 3 falls short but candle 4 breaks candle 1's closing and candle 2's opening price. We can enter on candle 4.

3. We need to enter the trade as soon as the price moves below the candle 1 and 2's body and should not wait for the 3rd or 4th candle to close.

4. But for a more optimised entry I have added an option to use candle’s highs and lows instead of open and close. This reduces lot of noise and provides us with more precise entry. This setting is turned on by default.

5. I have restricted it to 4 candles and that is all that is needed. More than that is a longer sideways market.

6. I call it the -+- or RGR pattern or Red-Green-Red or Seller-Buyer-Seller or Buyer defeated or just Seller pattern.

7. Stop loss can be candle 2's mid for safe traders ( that includes me) or candle 2's body high for risky traders.

8. Back testing suggests that body high will be useless and result in more points in loss because for the bigger move this point will not be touched, so why not get out faster.

Combining Indicators and Signal

Combining these indicators with GRG/RGR signal can be very powerful and can provide big moves.

1. MA crossover and Signal - This is very powerful and provides a very big move. Trades can be held for longer. If after taking the trade we notice that the MA crossover has happened then trades can be held for higher targets.

2. Pivots and Signal - Pivots and add a support or resistance point. Take profits on these points. R5/S5 are over streched conditions so we can start looking for reversal signals and ignore other signals

3. Intraday Range - first 1, 5, 15 min of the day - Sideways days is when price will stay in these ranges. You can take profits at these ranges or if the range is broken and we get a signal, then it can mean that the direction will be sustained.

4. Previous Day/Week/Month Ranges - These can be used as Take Profit points if the price is moving towards them after getting the signal. If the range is broken and we get a signal then it can be a strong signal. They can also be used as reversal points if a strong signal is generated.

Important Settings

1. Include 4th Candle Confirmation - You can enable or disable the 4th candle signal to avoid the noise, but at times I have noticed that the 4th candle gives a very strong signal or I can say that the strong signal falls on the 4th candle. This is mostly a coincidence.

2. Bars to check (default 10) - You can also configure how many previous bars should the signal be generated for. 10 to 30 is good enough. To backtest increase it to 2000 or 5000 for example.

3. Use Candle High/Low for confirmation instead of Candle Open/Close - More optimized entry and noise reduction. This option is now defaulted to false.

4. Show Green-Red-Green (bull) signals - Show only bull entries. Useful when I have a predefined view i.e, I know market is going to go up today.

5. Show Red-Green-Red (bear) signals - Show only bear entries. Useful when I have a predefined view i.e, I know market is going to go down today.

6. 3rd candle should be a Strong candle before considering 4th candle - This will enforce additional logic in 4 candle setup that the 3rd candle is the candle in our direction of breakout. This means something like GRGG is mandatory, which is still the default behaviour. If disabled, the 3rd candle can be any candle and 4th candle will act as our breakout candle. This behaviour has led to breakouts and breakdowns as times, hence I added this as a separate feature. Vice-versa for a RGGR.

For a 4 candle setup till now we were expecting GRGG or RGRR but we can let the system ignore the 3rd candle completely if needed.

This will result in additional signals.

7. Three intraday ranges added for index and stock traders - 1 min, 5 min and 15 min ranges will be displayed. These are disabled by default except 15 min. These are very important ranges and in sideways days the price will usually move within the 15 min. A breakout of this range and a positive signal can be a very powerful setup.

Safe traders can avoid taking a trade in this range as it can lead to fakeouts.

The line style, width, color and opacity are configurable.

Pointers/Golden Rules

1. If after taking the trade, the next candle moves in your direction and closes strong bullish or bearish, then move SL to break even and after that you can trail it.

2. If a upside trade hits SL and immediately a down side trade signal is generated on the next candle then take it. Vice versa is true.

3. Trades need to be taken on previous 2 candle's body high or low combined and not the wicks.

4. The most losses a trader takes is on a sideways day and because in our strategy the stop loss is so small that even on a sideways day we'll get out with a little profit or worst break even.

5. Hold trades for longer targets and don't panic.

6. If last 3-4 days have been sideways then there is a good probability that today will be trending so we can hold our trade for longer targets. Inverse is true when the market has been trending for 2-3 days then volatility followed by sideways is coming (DOW theory). Target to hold the trade for whole day and not exit till the day closes.

7. In general avoid trading in the middle of the day for index and stocks. Divide the day into 3 parts and avoid the middle.

8. Use Support/Resistance, 10, 20, 50, 200 EMA/SMA, Gaps, Whole/Round numbers(very imp) for identifying targets.

9. Trail your SL.

10. For indexes I would use 5 min and 15 min timeframe and at times 10 mins.

11. For commodities and crypto we can use higher timeframe as well. Look for signals during volatile time durations and avoid trading the whole day. Signal usually gives good targets on those times.

12. If a GRG or RGR pattern appears on a daily timeframe then this is our time to go big.

13. Minimum Risk to Reward should be 1:2 and for longer targets can be 1:4 to 1:10.

14. Trade with small lot size. Money management will happen automatically.

15. With small lot size and correct Risk-Reward we can be very profitable. Don't trade with big lot size.

16. Stay in the market for longer and collect points not money.

17. Very imp - Watch market and learn to generate a market view.

18. Very imp - Only 3 type of candles are needed in trading -

Strong Bullish (Big Green candle), Strong Bearish (Big Red candle),

Hammer (it is Strong Bullish), Inverse Hammer (it is Strong Bearish)

and Doji (indecision or confusion).

If on daily timeframe I see Strong Bullish candle previous day then I am biased to the upside the next day, if I see Strong Bearish candle the previous day then I am biased to the downside the next day, if I see Doji on the previous day then I am cautious the next day, if there are back to back Dojis forming in daily or weekly then I am preparing for big move so time to go big once I get the signal.

19. Most Important Candlestick pattern - Bullish and Bearish Engulfing

20. The only Chart patterns I need -

a) Falling Wedge/Channel Bullish Pattern Uptrend or Bull Flag - Buying - Forming over a couple days for intraday and forming over a couple of weeks for swing

b) Falling Wedge/Channel Bullish Pattern Downtrend or Falling Channel - Buying

c) Rising Wedge Bearish Pattern Uptrend or Rising Channel - Selling

d) Rising Wedge Bearish Pattern Downtrend or Bear flag - Selling

e) Head and Shoulder - Over a longer period not for intraday. In 15 min takes few days and for swing 1hr or 4h or daily can take few days

f) M and W pattern - Reversal Patterns - They form within the above 4 patterns, usually resulting in the break of trend line

21. How Gaps work -

a) Small Gap up in Uptrend - Market can fill the gap and reverse. The perception is that people are buying. If previous day candle was Strong Bullish then market view is up.

b) Big Gap up in Uptrend - Not news driven - Profit booking will come but may not fill the entire gap

c) Big Gap up in Uptrend - News driven, war related, tax, interest rate - Market can keep going up without stopping.

c) Flat opening in Uptrend - Big chance of market going up. If previous day candle was Strong Bullish then view is upwards, if it was Doji then still upwards.

d) Gap down in Uptrend - Market is surprised. After going down initially it can go up

e) Small Gap down in Downtrend - Market can fill the gap and keep moving down. If previous day candle was Strong Bearish then view is still down.

f) Flat opening in Downtrend - View is down, short today.

g) Big Gap down in Downtrend - Profit booking and foolish buying will come but market view is still down.

h) Gap down with News - Volatility, sideways then down.

i) Gap Up in Downtrend - Can move up - Price can move up during 2/3rd of the day and End of the day revert and close in red.

22. Go big on bearish days for option traders. Puts are better bought and Calls are better sold.

23. Cluster of green signals can lead to bigger move on the upside and vice versa for red signals.

24. Most of this is what I learned from successful traders (from the top 2%) only the indicator is mine.

3/4-Bar GRG / RGR Pattern (Conditional 4th Candle)This indicator can be used to identify the Green-Red-Green or Red-Green-Red pattern.

It is a price action indicator where a price action which identifies the defeat of buyers and sellers.

If the buyers comprehensively defeat the sellers then the price moves up and if the sellers defeat the buyers then the price moves down.

In my trading experience this is what defines the price movement.

It is a 3 or 4 candle pattern, beyond that i.e, 5 or more candles could mean a very sideways market and unnecessary signal generation.

How does it work?

Upside/Green signal

Say candle 1 is Green, which means buyers stepped in, then candle 2 is Red or a Doji, that means sellers brought the price down. Then if candle 3 is forming to be Green and breaks the closing of the 1st candle and opening of the 2nd candle, then a green arrow will appear and that is the place where you want to take your trade.

Here the buyers defeated the sellers.

Sometimes candle 3 falls short but candle 4 breaks candle 1's closing and candle 2's opening price. We can enter on candle 4.

Important - We need to enter the trade as soon as the price moves above the candle 1 and 2's body and should not wait for the 3rd or 4th candle to close. Ignore wicks.

I have restricted it to 4 candles and that is all that is needed. More than that is a longer sideways market.

I call it the +-+ or GRG pattern.

Stop loss can be candle 2's mid for safe traders (that includes me) or candle 2's body low for risky traders.

Back testing suggests that body low will be useless and result in more points in loss because for the bigger move this point will not be touched, so why not get out faster.

Downside/Red signal

Say candle 1 is Red, which means sellers stepped in, then candle 2 is Green or a Doji, that means buyers took the price up. Then if candle 3 is forming to be Red and breaks the closing of the 1st candle and opening of the 2nd candle then a Red arrow will appear and that is the place where you want to take your trade.

Sometimes candle 3 falls short but candle 4 breaks candle 1's closing and candle 2's opening price. We can enter on candle 4.

We need to enter the trade as soon as the price moves below the candle 1 and 2's body and should not wait for the 3rd or 4th candle to close.

I have restricted it to 4 candles and that is all that is needed. More than that is a longer sideways market.

I call it the -+- or RGR pattern.

Stop loss can be candle 2's mid for safe traders ( that includes me) or candle 2's body high for risky traders.

Back testing suggests that body high will be useless and result in more points in loss because for the bigger move this point will not be touched, so why not get out faster.

Important Settings

You can enable or disable the 4th candle signal to avoid the noise, but at times I have noticed that the 4th candle gives a very strong signal or I can say that the strong signal falls on the 4th candle. This is mostly a coincidence.

You can also configure how many previous bars should the signal be generated for. 10 to 30 is good enough. To backtest increase it to 2000 or 5000 for example.

Rest are self explanatory.

Pointers

If after taking the trade, the next candle moves in your direction and closes strong bullish or bearish, then move SL to break even and after that you can trail it.

If a upside trade hits SL and immediately a down side trade signal is generated on the next candle then take it. Vice versa is true.

Trades need to be taken on previous 2 candle's body high or low combined and not the wicks.

The most losses a trader takes is on a sideways day and because in our strategy the stop loss is so small that even on a sideways day we'll get out with a little profit or worst break even.

Hold targets for longer targets and don't panic.

If last 3-4 days have been sideways then there is a good probability that day will be trending so we can hold our trade for longer targets. Target to hold the trade for whole day and not exit till the day closes.

In general avoid trading in the middle of the day for index and stocks. Divide the day into 3 parts and avoid the middle.

Use Support/Resistance, 10, 20, 50, 200 EMA/SMA, Gaps, Whole/Round numbers(very imp) for identifying targets.

Trail your SL.

For indexes I would use 5 min and 15 min timeframe.

For commodities and crypto we can use higher timeframe as well. Look for signals during volatile time durations and avoid trading the whole day. Signal usually gives good targets on those times.

If a GRG or RGR pattern appears on a daily timeframe then this is our time to go big.

Minimum Risk to Reward should be 1:2 and for longer targets can be 1:4 to 1:10.

Trade with small lot size. Money management will happen automatically.

With small lot size and correct Risk-Re ward we can be very profitable. Don't trade with big lot size.

Stay in the market for longer and collect points not money.

Very imp - Watch market and learn to generate a market view.

Very imp - Only 4 candles are needed in trading - strong bullish, strong bearish, hammer, inverse hammer and doji.

Go big on bearish days for option traders. Puts are better bought and Calls are better sold.

Cluster of green signals can lead to bigger move on the upside and vice versa for red signals.

Most of this is what I learned from successful traders (from the top 2%) only the indicator is mine.

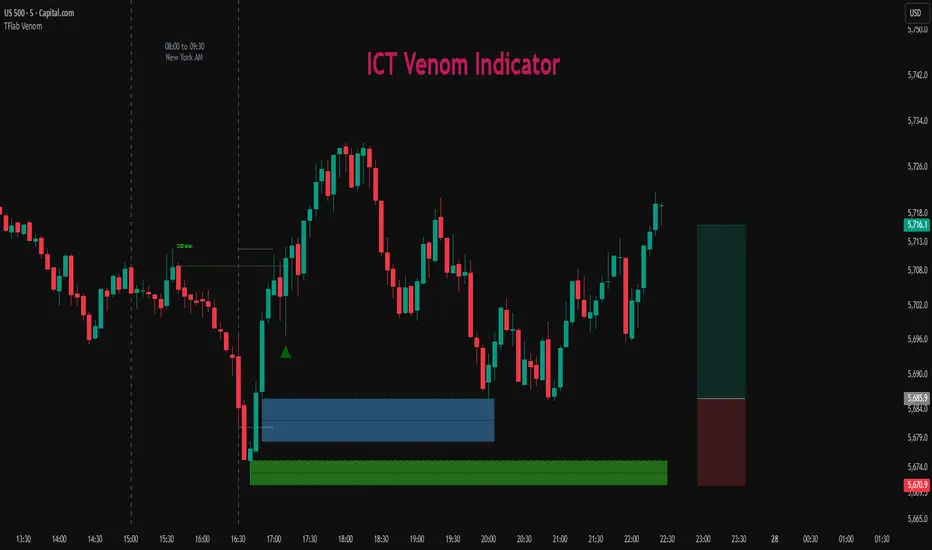

ICT Venom Trading Model [TradingFinder] SMC NY Session 2025SetupIntroduction

The ICT Venom Model is one of the most advanced strategies in the ICT framework, designed for intraday trading on major US indices such as US100, US30, and US500. This model is rooted in liquidity theory, time and price dynamics, and institutional order flow.

The Venom Model focuses on detecting Liquidity Sweeps, identifying Fair Value Gaps (FVG), and analyzing Market Structure Shifts (MSS). By combining these ICT core concepts, traders can filter false breakouts, capture sharp reversals, and align their entries with the real institutional liquidity flow during the New York Session.

Key Highlights of ICT Venom Model :

Intraday focus : Optimized for US indices (US100, US30, US500).

Time element : Critical window is 08:00–09:30 AM (Venom Box).

Liquidity sweep logic : Price grabs liquidity at 09:30 AM open.

Confirmation tools : MSS, CISD, FVG, and Order Blocks.

Dual setups : Works in both Bullish Venom and Bearish Venom conditions.

At its core, the ICT Venom Strategy is a framework that explains how institutional players manipulate liquidity pools by engineering false breakouts around the initial range of the market. Between 08:00 and 09:30 AM New York time, a range called the “Venom Box” is formed.

This range acts as a trap for retail traders, and once the 09:30 AM market open occurs, price usually sweeps either the high or the low of this box to collect stop-loss liquidity. After this liquidity grab, the market often reverses sharply, giving birth to a classic Bullish Venom Setup or Bearish Venom Setup

The Venom Model (ICT Venom Trading Strategy) is not just a pattern recognition tool but a precise institutional trading model based on time, liquidity, and market structure. By understanding the Initial Balance Range, watching for Liquidity Sweeps, and entering trades from FVG zones or Order Blocks, traders can anticipate market reversals with high accuracy. This strategy is widely respected among ICT followers because it offers both risk management discipline and clear entry/exit conditions. In short, the Venom Model transforms liquidity manipulation into actionable trading opportunities.

Bullish Setup :

Bearish Setup :

🔵 How to Use

The ICT Venom Model is applied by observing price behavior during the early hours of the New York session. The first step is to define the Initial Range, also called the Venom Box, which is formed between 08:00 and 09:30 AM EST. This range marks the high and low points where institutional traders often create traps for retail participants. Once the official market opens at 09:30 AM, price usually sweeps either the top or bottom of this box to collect liquidity.

After this liquidity grab, the market tends to reverse in alignment with the true directional bias. To confirm the setup, traders look for signals such as a Market Structure Shift (MSS), Change in State of Delivery (CISD), or the appearance of a Fair Value Gap (FVG). These elements validate the reversal and provide precise levels for trade execution.

🟣 Bullish Setup

In a Bullish Venom Setup, the market first sweeps the low of the Venom Box after 09:30 AM, triggering sell-side liquidity collection. This downward move is often sharp and deceptive, designed to stop out retail long positions and attract new sellers. Once liquidity is taken, the market typically shifts direction, forming an MSS or CISD that signals a reversal to the upside.

Traders then wait for price to retrace into a Fair Value Gap or a demand-side Order Block created during the reversal leg. This retracement offers the ideal entry point for long positions. Stop-loss placement should be just below the liquidity sweep low, while profit targets are set at the Venom Box high and, if momentum continues, at higher session or daily highs.

🟣 Bearish Setup

In a Bearish Venom Setup, the process is similar but reversed. After the Initial Range is defined, if price breaks above the Venom Box high following the 09:30 AM open, it signals a false breakout designed to collect buy-side liquidity. This move usually traps eager buyers and clears out stop-losses above the high.

After the liquidity sweep, confirmation comes through an MSS or CISD pointing to a reversal downward. At this stage, traders anticipate a retracement into a Fair Value Gap or a supply-side Order Block formed during the reversal. Short entries are taken within this zone, with stop-loss positioned just above the liquidity sweep high. The logical profit targets include the Venom Box low and, in stronger bearish momentum, deeper session or daily lows.

🔵 Settings

Refine Order Block : Enables finer adjustments to Order Block levels for more accurate price responses.

Mitigation Level OB : Allows users to set specific reaction points within an Order Block, including: Proximal: Closest level to the current price. 50% OB: Midpoint of the Order Block. Distal: Farthest level from the current price.

FVG Filter : The Judas Swing indicator includes a filter for Fair Value Gap (FVG), allowing different filtering based on FVG width: FVG Filter Type: Can be set to "Very Aggressive," "Aggressive," "Defensive," or "Very Defensive." Higher defensiveness narrows the FVG width, focusing on narrower gaps.

Mitigation Level FVG : Like the Order Block, you can set price reaction levels for FVG with options such as Proximal, 50% OB, and Distal.

CISD : The Bar Back Check option enables traders to specify the number of past candles checked for identifying the CISD Level, enhancing CISD Level accuracy on the chart.

🔵 Conclusion

The ICT Venom Model is more than just a reversal setup; it is a complete intraday trading framework that blends liquidity theory, time precision, and market structure analysis. By focusing on the Initial Range between 08:00 and 09:30 AM New York time and observing how price reacts at the 09:30 AM open, traders can identify liquidity sweeps that reveal institutional intentions.

Whether in a Bullish Venom Setup or a Bearish Venom Setup, the model allows for precise entries through Fair Value Gaps (FVGs) and Order Blocks, while maintaining clear risk management with well-defined stop-loss and target levels.

Ultimately, the ICT Venom Model provides traders with a structured way to filter false moves and align their trades with institutional order flow. Its strength lies in transforming liquidity manipulation into actionable opportunities, giving intraday traders an edge in timing, accuracy, and consistency. For those who master its logic, the Venom Model becomes not only a strategy for entry and exit, but also a deeper framework for understanding how liquidity truly drives price in the New York session.

Intraday Momentum for Volatile Stocks 29.09The strategy targets intraday momentum breakouts in volatile stocks when the broader market (Nifty) is in an uptrend. It enters long positions when stocks move significantly above their daily opening price with sufficient volume confirmation, then manages the trade using dynamic ATR-based stops and profit targets.

Entry Conditions

Price Momentum Filter: The stock must move at least 2.5% above its daily opening price, indicating strong bullish momentum. This percentage threshold is customizable and targets gap-up scenarios or strong intraday breakouts.

Volume Confirmation: Daily cumulative volume must exceed the 20-day average volume, ensuring institutional participation and genuine momentum. This prevents false breakouts on low volume.

Market Regime Filter: The Nifty index must be trading above its 50-day SMA, indicating a favorable market environment for momentum trades. This macro filter helps avoid trades during bearish market conditions.

Money Flow Index: MFI must be above 50, confirming buying pressure and positive money flow into the stock. This adds another layer of momentum confirmation.

Time Restriction: Trades are only initiated before 3:00 PM to ensure sufficient time for position management and avoid end-of-day volatility.

Exit Management

ATR Trailing Stop Loss: Uses a 3x ATR multiplier for dynamic stop-loss placement that trails higher highs, protecting profits while giving trades room to breathe. The trailing mechanism locks in gains as the stock moves favorably.

Profit Target: Set at 4x ATR above the entry price, providing a favorable risk-reward ratio based on the stock's volatility characteristics. This adaptive approach adjusts targets based on individual stock behavior.

Position Reset: Both stops and targets reset when not in a position, ensuring fresh calculations for each new trade.

Key Strengths

Volatility Adaptation: The ATR-based approach automatically adjusts risk parameters to match current market volatility levels. Higher volatility stocks get wider stops, while calmer stocks get tighter management.

Multi-Timeframe Filtering: Combines intraday price action with daily volume patterns and market regime analysis for robust signal generation.

Risk Management Focus: The strategy prioritizes capital preservation through systematic stop-loss placement and position sizing considerations.

Considerations for NSE Trading

This strategy appears well-suited for NSE intraday momentum trading, particularly for mid-cap and small-cap stocks that exhibit high volatility. The Nifty filter helps align trades with broader market sentiment, which is crucial in the Indian market context where sectoral and index movements strongly influence individual stocks.

The 2.5% threshold above open price is appropriate for volatile NSE stocks, though traders might consider adjusting this parameter based on the specific stocks being traded. The strategy's emphasis on volume confirmation is particularly valuable in the NSE environment where retail participation can create misleading price movements without institutional backin

Katz Impact Wave 🚀Overview of the Katz Impact Wave 🚀